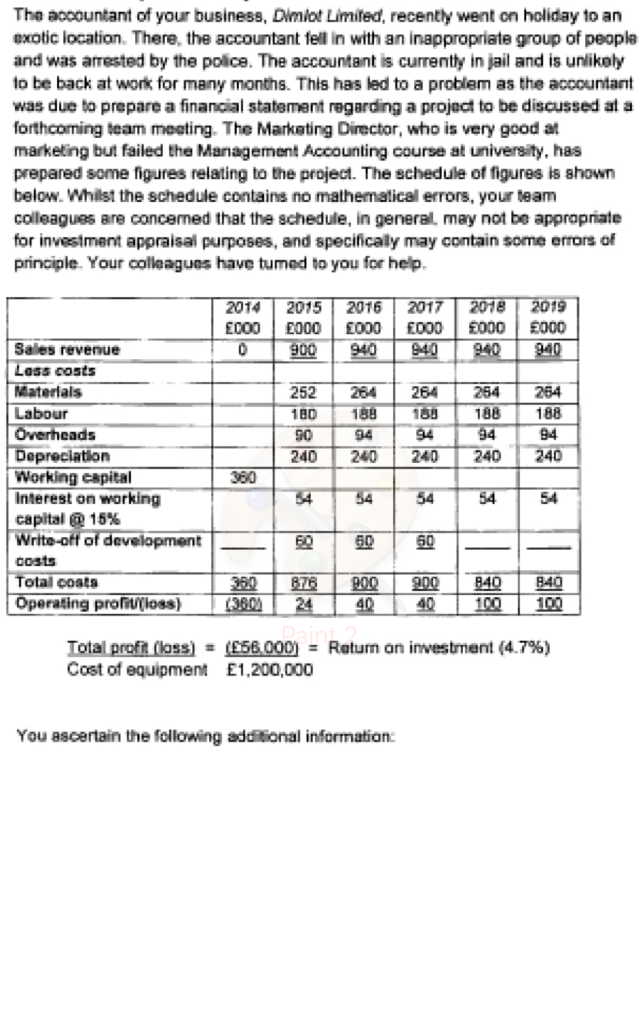

Show transcribed image text The accountant of your business, Dimiot Limired, recently went cn holiday to an exotic location. There, the accountant fell in with an inappropriate group ofpeople and was arrested by the police. The accountant is currently in jail and is unlikely to be back at work for many months. This has led to a problem as the accountant was due to prepare a financial statement regarding a project to be discussed at a forthcoming team meeting. The Marketing Director, who is very good at marketing but failed the Management Accounting course at university, has prepared some figures relating to the project. The schedule of figures is shown below. Whilst the schedule contains no mathematical errors, your team colleagues are concermed that the schedule, in general. may not be appropriate for investment appraisal purposes, and specifically may contain some errors of principle. Your colleagues have tumed to you for help. 2014 2015 2016 2017 2018 2019 E000 E000 1000 E000 E000 E000 Sales revenue Loss costs Materials 252 264 264 264 264 Labour 18D 18 188 18 188 Overheads Depreciation 240 240 240 240 240 Working capital interest on working capital 15% Write-off of development 90 Costs Total costs 200 200 840 840 Operating profit(ioss) K320M 24 40 40 100 102 Total profit (loss) (E58 000a Return on investment (4.7%) Cost of equipment E1,200,000 You ascertain the following additional information:

The accountant of your business, Dimiot Limired, recently went cn holiday to an exotic location. There, the accountant fell in with an inappropriate group ofpeople and was arrested by the police. The accountant is currently in jail and is unlikely to be back at work for many months. This has led to a problem as the accountant was due to prepare a financial statement regarding a project to be discussed at a forthcoming team meeting. The Marketing Director, who is very good at marketing but failed the Management Accounting course at university, has prepared some figures relating to the project. The schedule of figures is shown below. Whilst the schedule contains no mathematical errors, your team colleagues are concermed that the schedule, in general. may not be appropriate for investment appraisal purposes, and specifically may contain some errors of principle. Your colleagues have tumed to you for help. 2014 2015 2016 2017 2018 2019 E000 E000 1000 E000 E000 E000 Sales revenue Loss costs Materials 252 264 264 264 264 Labour 18D 18 188 18 188 Overheads Depreciation 240 240 240 240 240 Working capital interest on working capital 15% Write-off of development 90 Costs Total costs 200 200 840 840 Operating profit(ioss) K320M 24 40 40 100 102 Total profit (loss) (E58 000a Return on investment (4.7%) Cost of equipment E1,200,000 You ascertain the following additional information: